{kind=link}

A new poll conducted for MNP LTD by Ipsos shows that many Canadians have little financial flexibility from month to month and that rising interest rates already have many Canadians worried about their financial future.

Money Remaining After Bills and Debt Payments

After paying bills and debt payments, the average Canadian has $630 left over but 33% of Canadians actually have nothing left over. Interestingly, there is a fairly clear East-West divide in what is left. The further West you live the more money you have left after you pay your bills and debt payments.

The East-West gradient is not as clear when one looks at the share of the population that has nothing left, what the survey calls insolvency. Overall 33% of Canadians fall into that category.

Those in B.C. are the least likely (25%) and Quebec the most likely (39%) to report having nothing left but Ontario, the Prairies, and Alberta are all about the same level despite the significant difference in the mean. This would suggest that there is a bigger gap between those who have nothing and those who have money left over in Alberta compared with the Prairies and Ontario.

Additionally, it is interesting that 27% of those who have a household mortgage have nothing left compared with 20% who own their home outright. Those who do not own a home are the most likely to have nothing left (45%).

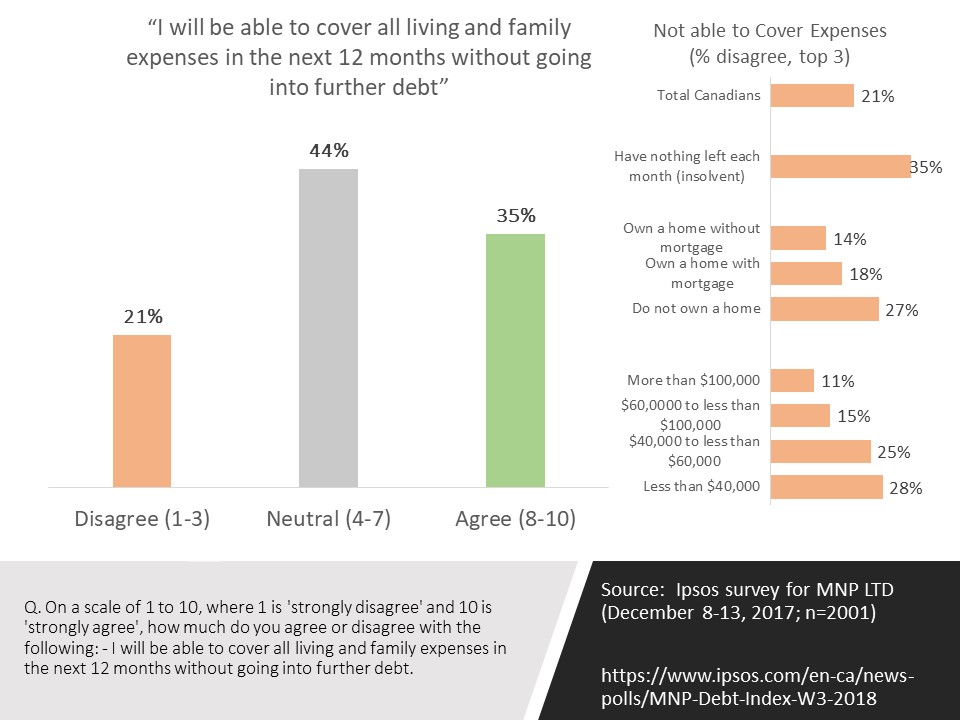

Ability to Pay Expenses without Additional Debt

A good indicator of the fragility of personal finances is the extent to which people anticipate being able to cover all their living an family expenses without going into further debt. Just 35% are confident (they are 8-10 on the agree scale) they will be able to do so and 21% are not confident (bottom 3, 1-3 on the scale).

The proportion not able to pay is 21% overall but it is 35% of those who currently live month to month with nothing left over. It is also higher for those who don’t own a home (though not much higher for those who have a mortgage versus those who don’t) and for those with less household income.

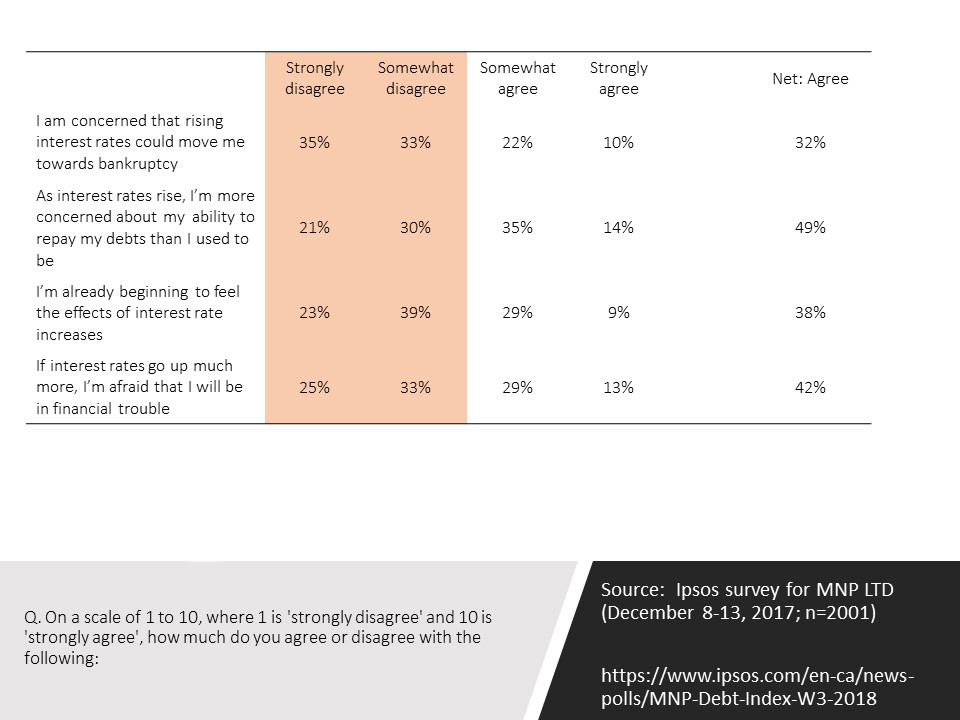

Interest Rates

Given economic growth and employment strength in Canada, the big risk to consumers is the rising cost of borrowing that will result from these other strengths. Included in the survey were four questions which tapped directly into interest rate concern. Certainly many Canadians are concerned.

The highest level of agreement is to the softest question in that 49% say that they are more concerned about their ability to repay their debts as interest rates rise. Of course, only 14% feel strongly. This still represents a significant level of concern that is reflected in the agreement to the other questions.

Consider the fact that 42% agree (13%) strongly that if interest rates go up, they are afraid they will be in financial trouble. importantly, this is even higher (49%, 14% strongly) among those who have a mortgage and those who have nothing left over after they pay with monthly bills (63%, 24% strongly).

Source: An online survey was conducted for MNP LTD between December 8 and 13th, 2017 (n=2001). Additional information available at Ipsos.